Self-Driving Car Fleets: Transportation As A Service

The automotive industry is an anomaly. The industry has annual worldwide sales of over $1.5 trillion. It’s dominated by a dozen powerful conglomerates each with distinct consumer brands. And, so far, it’s almost completely avoided the digital age and the effects this new age has on business models. All three of these unique traits will change over the next decade.

The rise of self-driving cars will remake the automotive industry, devastating most companies, and enriching a small few. Fortunately, there are many lessons from other industries that we can apply to understand what will likely happen in this new transportation industry.

Before diving into that, we first need to understand why the future of transportation is self-driving car fleets. I won’t spend much time on the topic as it’s been talked about extensively elsewhere, but it’s important to understand so we can build upon it later.

Currently, the average personal car utilization rate is ~5%. Under a well-optimized system, fleet self-driving vehicles could have a utilization rate of 50%+. This higher utilization means a lower cost to the end consumer.

Deloitte estimates that a personally owned vehicle costs ~$0.97 per mile and a self-driving car in a fleet will cost ~$0.30 per mile. Assuming a person drives 10,000 miles per year, that’s an annual savings of $6,700. These savings alone will likely be enough to convince large amounts of the population to switch to a Transportation as a Service (TaaS) system. Additionally, governments will likely see the safety and environmental benefits of self-driving fleets and in turn, disincentivize personal car ownership to help convince more people to switch.

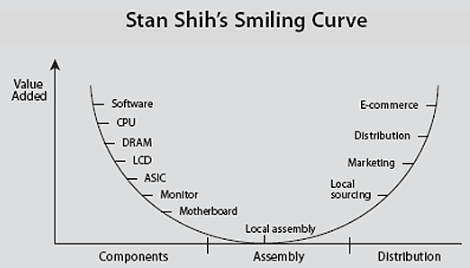

To understand how this new model will change the automotive industry, we can look at the personal computer (PC) and mobile industries. These industries have experienced significant changes over the last 30 years, but there has been one constant pattern throughout that time: the Smiling Curve.

The Smiling Curve was created by Acer (a computer OEM firm) founder Stan Shih in 1992. The theory illustrates that the ends of the computer value chain command a higher value add. For instance, both Windows, who creates the software, and Intel, who owns the R&D for the main computer microchips, are able to capture most of the profit in the PC industry. The rest of the industry players are forced to compete for the leftovers.

/http%3A%2F%2F1.bp.blogspot.com%2F-9q2UVZx-9WY%2FXzSC9xT3vMI%2FAAAAAAAAOXg%2FV5fWOj9W7mY9v0k6dLmohbYqsfFEM9sCgCLcBGAsYHQ%2Fw589-h393%2F9720011865_8a9109d2bf_o.jpg)

/http%3A%2F%2Fcdn.vox-cdn.com%2Fthumbor%2F_8W9-BYpT4-qtFafgdymfFL_BTk%3D%2F0x0%3A2048x1182%2F1200x800%2Ffilters%3Afocal%28488x541%3A814x867%29%2Fcdn.vox-cdn.com%2Fuploads%2Fchorus_image%2Fimage%2F66473678%2FEStvCm0WsAEbMCX.0.jpg)

/http%3A%2F%2F9q6pu33arq33jokx6qglbp6n-wpengine.netdna-ssl.com%2Fwp-content%2Fuploads%2F2017%2F05%2FThe-Self-Driving-Car-Timeline-950x540.jpg)

/http%3A%2F%2Fcdn.vox-cdn.com%2Fthumbor%2FMPYHgp4_uIl0aeiY5B7EBFSVBFs%3D%2F0x0%3A2559x1664%2F1200x800%2Ffilters%3Afocal%281076x628%3A1484x1036%29%2Fcdn.vox-cdn.com%2Fuploads%2Fchorus_image%2Fimage%2F66122889%2F1189070708.jpg.0.jpg)