U.S. Connected Car Market Overview

U.S. Connected Car Market Overview

A connected car is a car which is equipped with internet access, and has the ability to optimize its own operations on fixed intervals. The network connectivity permits the car to share content with a range of devices lying within and outside the vehicle’s environment. The various applications of network connectivity include navigation, telematics, and infotainment.

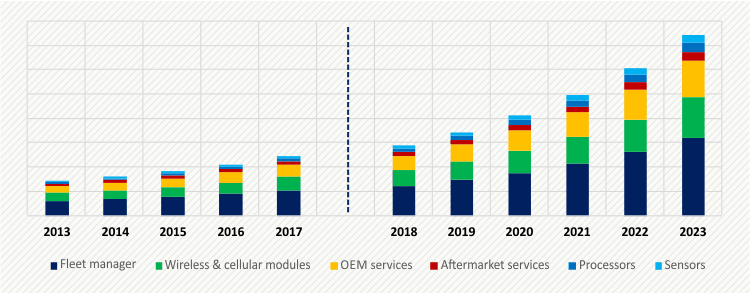

Based on products and services segment, the U.S. connected car market is categorized into fleet manager, wireless and cellular modules, OEM services, aftermarket services, processors, and sensors. Of these, fleet manager held the largest share in the U.S. market in 2017. This category is growing owing to the adoption of connected car technologies, primarily tracking of vehicles in the fleet by fleet managers. Such technologies help fleet managers to track the vehicle condition and do vehicle maintenance before the occurrence of any serious vehicle casualties.

Based on technology, the U.S. connected car market is categorized into 4G/LTE, 3G, and 2G. Among these, 4G/LTE technology is expected to be the fastest growing technology in the market, registering a CAGR of 23.8% during the forecast period. 4G/LTE technology enables consumers to quickly download files over a wireless network, and provides enhanced high voice quality, ease in usage of IM, social networks, streaming media, video calling, enhanced navigation system for the vehicle, and higher bandwidth.

Integrated category was the largest category in the connectivity segment in U.S. connected car market, holding 43.9% market share in 2017. The dominance of the integrated connectivity category can be owed to its compact structure and user-friendly characteristic nature.

U.S. Connected Car Market Dynamics

Trends

The emergence of AV technology in the U.S. connected car market is one of the key trends that is here to stay. The market has already witnessed advanced driver-assistance system (ADAS) solution which has changed the face of driving experience, making it safer than ever. Up until now, the automotive OEMs, in collaboration with their technology partners (for instance, BMW AG and NVIDIA Corporation; Volvo AB and Google LLC), have delivered significant breakthroughs in the market.

The technologies used in semi-autonomous vehicles, including adaptive front lighting system, lane-departure warning system, and surround view, have made the headway for the AV technology. Although, the AV technology is already being tested at working level under fixed circumstances, its commercial incorporation in cars is still underway. The growth and acceptance of such technology are predominantly dependent upon the hardware and software innovations. The hardware development is already approaching the level required for the AV technology to be commercialized, but the growing demand for related software to increase the driver experience is rising the attention toward software that needs to be upgraded to unlock the full potential of the AV technology and the hardware involved.

Read more : https://www.psmarketresearch.com/market-analysis/us-connected-car-market

/http%3A%2F%2F1.bp.blogspot.com%2F-9q2UVZx-9WY%2FXzSC9xT3vMI%2FAAAAAAAAOXg%2FV5fWOj9W7mY9v0k6dLmohbYqsfFEM9sCgCLcBGAsYHQ%2Fw589-h393%2F9720011865_8a9109d2bf_o.jpg)

/https%3A%2F%2Fassets.over-blog.com%2Ft%2Fcedistic%2Fcamera.png)

/http%3A%2F%2Fwww.marketsandmarkets.com%2FImages%2Fconnected-car-market4.jpg)

/http%3A%2F%2Fwww.marketsandmarkets.com%2FImages%2Fautomotive-vehicle-to-everything-v2x-market5.jpg)